Now you can invest in oceanfront real estate with as little as $1,000

Co-own a Nova Scotia beach destination through FrontFundr with Forge & Foster

Soaring real estate prices have locked many Canadians out of the market — and the wealth gains that come with ownership.

“For too long, real estate has been behind closed doors and not accessible to everyone,” says Joe Accardi, Partner & CEO of Forge & Foster. “We want to bring real estate to all Canadians, and FrontFundr is something that we’re really excited about.”

WHAT IS FRONTFUNDR?

FrontFundr is Canada’s leading online private markets investing platform and an exempt market dealer.

Founded in Vancouver in 2013, the startup’s mission is to democratize the private sector investment model by offering companies an alternative to venture and private equity investing.

FrontFundr provides investors with the opportunity to invest in startups and growth companies. Their online platform allows all Canadians — from professionals to first-time investors —to support the ideas and initiatives they want to see succeed.

The company has built up a community of over 34,000 users, run over 100 successful funding campaigns, and helped businesses raise more than $120 million so far.

“You might think you can only invest in Wealthsimple and public stocks, but you can also invest in early stage companies from the very beginning.”

“We’re missionaries to spread the word around equity crowdfunding, in general,” says Peter-Paul Van Hoeken, the founder and CEO of Silver Maple Ventures, FrontFundr’s parent company. “Creating awareness has been a huge job for our company in the last five years. You might think you can only invest in Wealthsimple and public stocks, but you can also invest in early stage companies from the very beginning.”

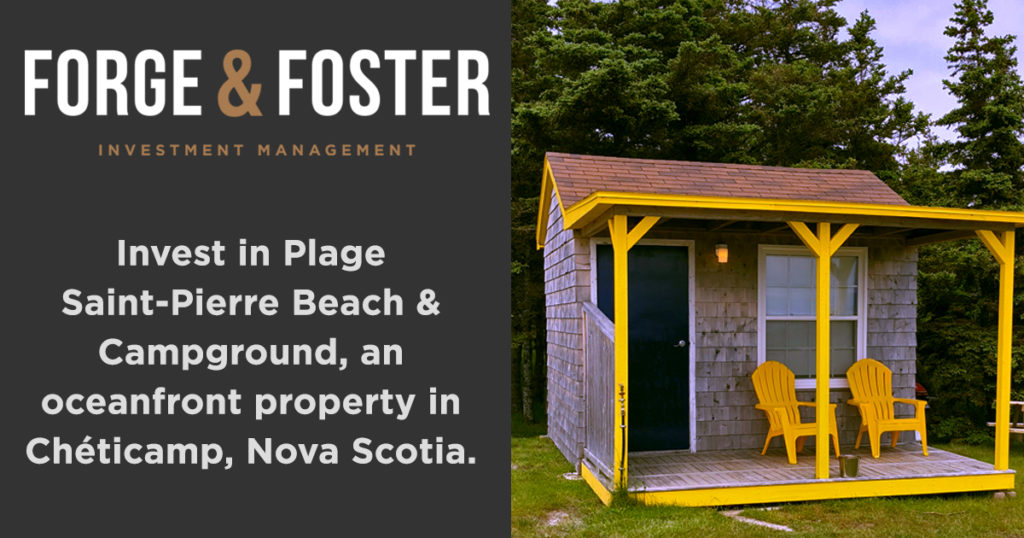

TELL ME ABOUT THE PROPERTY

The Plage Saint-Pierre Beach and Campground in Cheticamp, Nova Scotia, sits on 2,500 feet of private beach along one of the province’s warmest bays.

The nearby Cabot Cape Breton Golf Club is a popular destination. Visitors also enjoy hiking, whale watching, berry picking, stargazing, kayaking, cycling, dining on fresh seafood and more.

The popular destination boasts quaint cabins, RV rentals, and sites for tents and RVs. However, there is plenty of opportunity for improvement and expansion.

Situated at the gateway of the world-famous Cape Breton Highlands National Park and just off the Cabot Trail, this real estate investment property is packed with potential. And Forge & Foster is ready to unlock that potential through its unparalleled expertise in real estate management.

“Never before have people had the opportunity to invest in spectacular real estate like this, starting at just $1,000.”

Joe Accardi, Partner and CEO at Forge & Foster Investment Management, said, “This is a very special opportunity for investors and we’re excited to offer it through our trusted partner, FrontFundr. Never before have people had the opportunity to invest in spectacular real estate like this, starting at just $1,000.”

WHY FRONTFUNDR?

Here are the main benefits of investing in real estate through FrontFundr:

- No fees

- Pride of ownership

- No need to qualify for a mortgage

- No down payment required

- None of the pain of managing a property

- No closing costs

- No need to find tenants or maintain the property

- You’ll get a share of rent and gains on the property when it’s sold

- You’ll receive ongoing oversight and support

- Every investment project undergoes a detailed due diligence process

“Join FrontFundr. Take a look at their projects. You can invest in a project that you’re excited about,” says Accardi.

⭐⭐⭐⭐⭐

Great platform to invest in early stage enterprise

The investment process was straightforward and well explained.

—Jean-Philippe Deblois, Trust Pilot

⭐⭐⭐⭐⭐

Great platform that is intuitive and easy to use!

Good access to detailed prospectus and pitch info. The digital signing process is simple and efficient. Private company investing has never been this easy or accessible.

— Ken Smith, Trust Pilot

⭐⭐⭐⭐⭐

I feel fully confident that I am making sound investment decisions for myself. FrontFundr is an essential platform to democratize investing into early stage companies that have huge potential to add value.

— Leon Lie, Trust Pilot

WHAT ARE THE EXPERTS SAYING?

“Small investments in multiple projects add up over time. That makes it appealing for young people who want to get in the habit of investing.”

“I feel that real estate crowdfunding can be a viable tool for those who want to invest in real estate but are restricted due to a lack of money or credit,” says Mark Ting, CBC’s finance columnist. “Small investments in multiple projects add up over time. That makes it appealing for young people who want to get in the habit of investing.”

“A crowdfunded model comes with transparency and tangibility,” Tina Tehranchian, an Assante Capital Management Ltd. senior wealth adviser told the Globe and Mail. “You can drive by the property and boast to your friends that you have a share of ownership of this property.”

HOW DO I JOIN?

Sign up for FrontFundr now — there’s no fee to join!

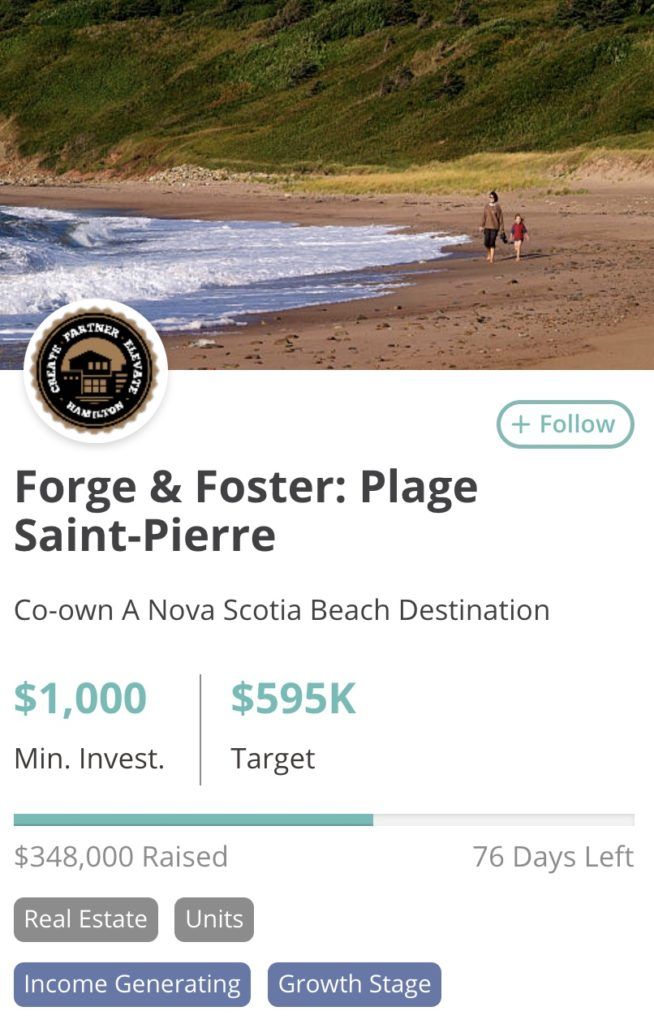

Plage Saint-Pierre Beach & Campground is currently raising $595,000. Details of the offering can be found at frontfundr.com/forgeandfoster.

To book a stay at Plage Saint-Pierre Beach & Campground, visit plagestpierre.com or contact plagesaintpierre@gmail.com or (902) 224-2112.