Investing in a Volatile Market: Strategies to Succeed

It’s no secret that the current market is incredibly volatile. Prices are bouncing all over the place, and it can be hard to know what’s the right thing to do when it comes to investing in your future.

In this blog post, we’ll go over some of the strategies you can use when investing in a volatile market, as well as some common mistakes people make during times like these.

So whether you’re a seasoned investor or just starting out, read on for some valuable insights!

what happens during periods of market volatility?

During periods of market volatility, prices tend to go up and down rapidly, making it hard to predict which way the market will move next. This can be a scary time for investors, as there is always the possibility of losing money. However, it’s important to remember that market volatility is normal and happens every few years.

When the stock market is volatile and inflation is on the rise, it can be difficult to know how to protect your investments. But there are some strategies you can use to help safeguard your portfolio.

Remember, there’s no “right” approach for everyone! The best strategy for you will depend on your individual circumstances and goals. Be sure to speak with a financial advisor so you can figure out a plan that works for you.

Invest in Success

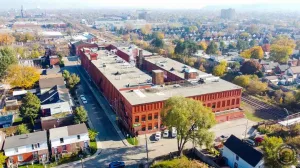

We’re honoured to carry on the tradition of performance as stewards of the historic Karma Candy Building at 356 Emerald St. N. in Hamilton, and we’re excited to invite you to join us as co-owners of this property through BuyProperly.

Learn Morethe top 6 strategies investors can use during a period of market instability

1. Diversify your Portfolio

One of the best ways to protect your investments during a volatile market is to diversify your portfolio.

It means investing in a variety of different asset types, including stocks, bonds, and cash. This will help to mitigate your risk if one particular asset class starts to decline. It also means investing in a variety of geographies and investing in products.

As an example, your portfolio may include a combination of stocks from different sectors, such as healthcare, tech, and finance, bonds with different maturity dates, or different countries, like Canada, the US, and Europe.

2. Consider Alternative Investments

Alternative investments can be a good way to diversify your portfolio and protect against inflation. Some examples include real estate trusts, commodities, and hedge funds.

3. Stay disciplined with your investing

It can be tempting to try to time the market during periods of volatility. Often, investors will veer off course in search of a great deal. However, this can be a recipe for disaster. The best way to approach investing during a volatile market is to stick to your investment plan and refrain from making impulsive decisions. Investing longer periods of time, years rather than months helps even out the ups and downs of the market, and realize market growth over the longer term.

4. Review your investment mix

As market conditions change, so should your investment mix. Regularly reviewing and rebalancing your portfolio will help ensure that your investments are properly diversified and aligned with your goals. This means selling off assets that have increased in value and buying more of the assets that have lost value.

By doing this, you ensure that your portfolio stays diversified and aligned with your investment.

For example, if you’re close to retirement, you may want to adjust your portfolio to be more conservative. On the other hand, if you have a longer time horizon, you may be able to weather the ups and downs of the market and take on a bit more risk.

5. Be prepared for market corrections

A market correction is when the stock market experiences a sharp decline. These declines are often seen as a normal part of the market cycle. However, they can be difficult to stomach if you’re not prepared for them. Learning how to ride out a market correction will help you stay the course when your investments start to decline.

6. Try dollar-cost averaging

This involves investing a fixed amount of money into security or securities at regular intervals. By buying these securities over time, you’ll be able to average out the price and reduce your overall risk. This technique can help smooth out the ups and downs of the market.

With these tips, you (and your investment portfolio) will be better prepared to handle any periods of economic instability!

here are the 10 mistakes to avoid when investing during a period of market VOLATILITY

1. don't try to time the market

People often do this when they think the market is about to crash and they want to sell before it does. But no one can predict the future, so this strategy is often unsuccessful. If your timing is wrong, you could lose a lot of money or miss out on a rebound.

2. Don't invest everything at once

When the market is volatile, it’s often best to invest gradually over time. This way, you’ll be able to average out the price and reduce your overall risk.

3. Don't put all your eggs in one basket

4. don't panic

5. don't try to guess the bottom

6. Don't get emotional about your investments

7. don't forget about the fees

8. I’m factor in your taxes

9. always stick to comfortable levels of risk

10. don't forget about your goals

When making investment decisions, it’s important to keep your long-term goals in mind. Don’t let the market dictate your decisions. Stick to your plan and stay the course.

The more you hold onto your long-term investment vision, the less likely you’ll be swayed by short-term market fluctuations.

Although it seems simple, keeping these strategies in mind will help you feel more secure as you invest and grow wealth for your future (especially when the market becomes unpredictable)!

Investing during periods of market volatility can be difficult, but there are some strategies you can use to help reduce your risk. By diversifying your investments, using dollar-cost averaging, and avoiding common mistakes, you’ll be in a better position to weather the storm.

By staying diversified, investing gradually, and focusing on your long-term goals, you’ll be well on your way to success.

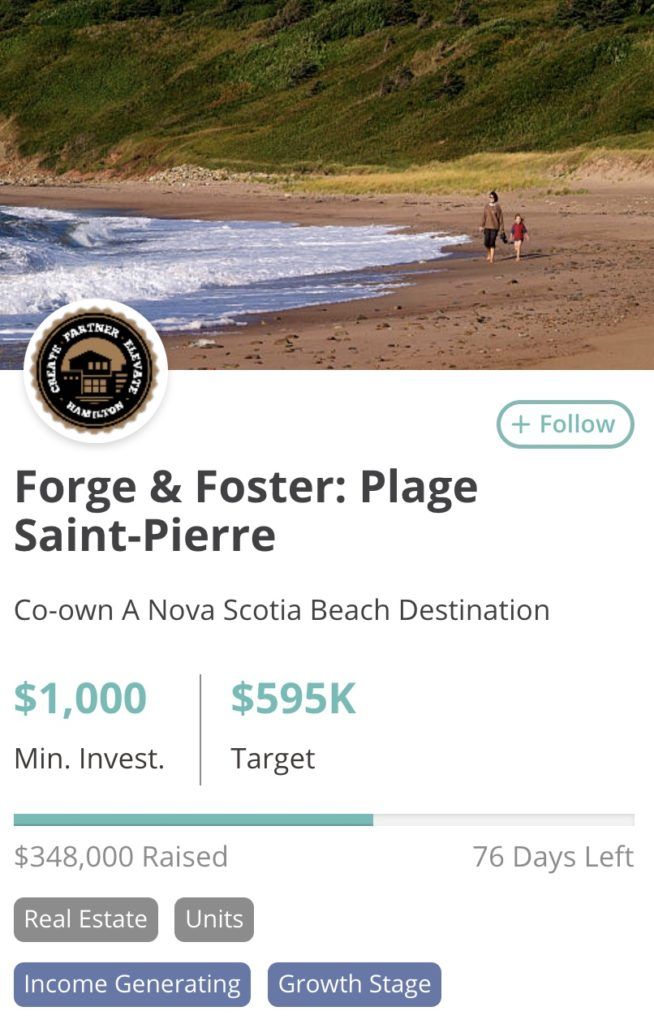

Looking to add to your real estate investment strategy? Learn more about our latest opportunity with BuyProperly.